How the Evolving News Economy Is Reshaping Investor Trust

Reputation, trust, and misinformation risk have moved to platforms and AI chatbots. What the Reuters Institute for the Study of Journalism 2026 Digital News Report mean for investor and technology company trust and reputation strategy.

AI and Reputation: Today's Biggest Geopolitical Risks?

Geopolitics, AI and governance are rewriting the rules of trust. Here's what new data from the 2026 Oxford University’s GlobeScan Global Corporate survey says, and why it matters to you.

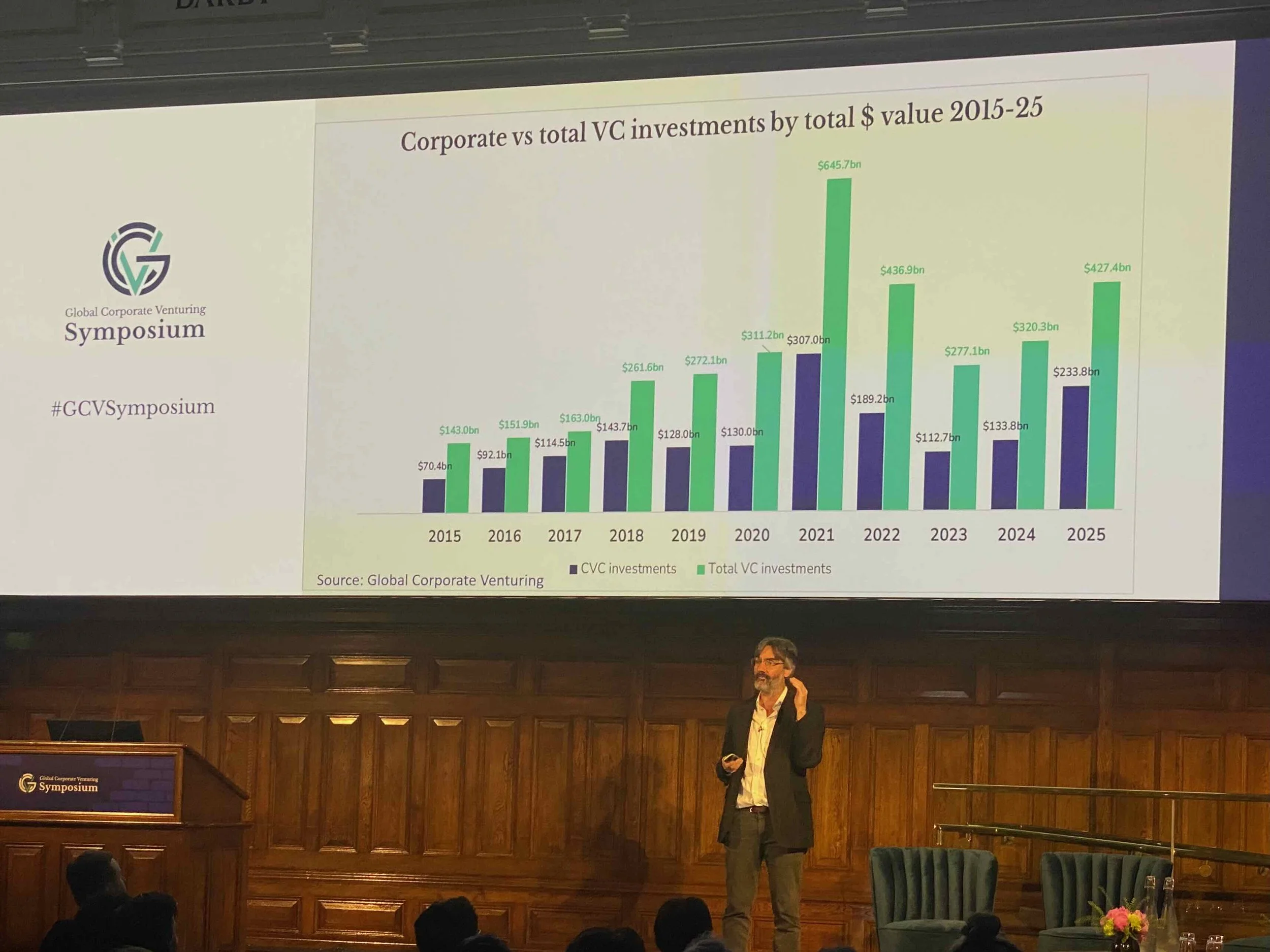

Corporate Venture Capital: The Human Innovation Gap

Two days at the Global Corporate Venturing Symposium in London confirmed something I have believed for years: the biggest barrier to innovation in investment, defence, and deep tech is not the technology. It is the risk-averse culture inside the institutions that should be accelerating it. Here is what the signals said, and why it matters now.

Why AI Companies Are Losing the Trust War

Two landmark global studies published this month reveal something the AI industry is not yet ready to hear. Public trust in AI is falling in the markets that matter most, and the information environment through which people form their opinions about it is in crisis. This is not a communications problem. It is a strategic one. Julio Romo draws on data from the Ipsos AI Monitor 2026 and the Reuters Institute Digital News Report 2026 to examine what the signals mean for AI companies, governments, and investors, and why tactical communications is making the trust deficit worse, not better.

Anthropic's Fable 5 Ban: The AI Sovereignty Wake-Up Call

The US just switched off Anthropic's most powerful AI models for the world. Here is what that means for every nation betting on AI for growth.

Why Now Is the Moment to Invest in UK Life Sciences Sector

The UK life sciences sector is backed by world-class science, £520 million in government commitments, and new private market infrastructure. So why is 94% of late-stage capital still coming from overseas?

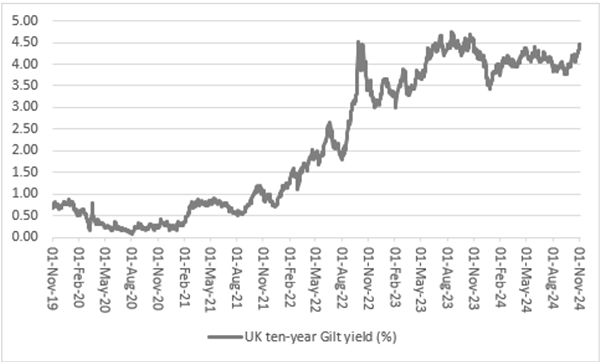

Why Bond Markets Are Not the Enemy of Governments

Bond markets are not the enemy of governments. They are the trustees of other people's futures, and they are asking one question that too many policy teams are failing to answer.

The Real Cost and Risk of Replacing Humans with AI

AI adoption is accelerating. So is the reputational and governance risk for organisations moving faster than the evidence supports

Why Media for Equity Is Going Global, and Why Now

Every startup needs advertising, marketing and promotion to grow. Media for equity is the instrument that lets founders buy reach without losing the cap table. Here is why it is going global, and why now.